Finance●Mid

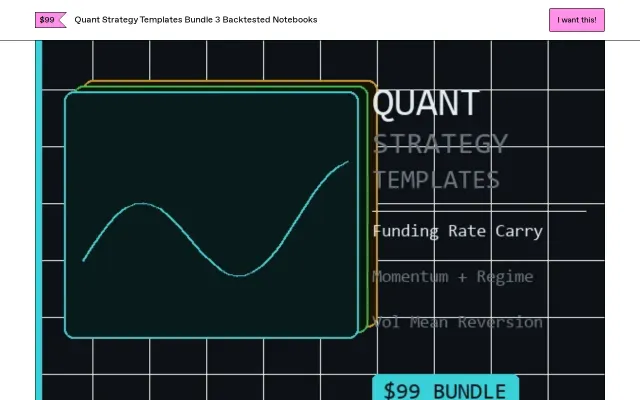

Three backtested quant strategies as Jupyter notebooks

$99 for Jupyter notebooks when QuantConnect and backtrader offer free backtesting frameworks.

Niche Gem

Shmungus

103mo ago

Rust backtesting engine with parallel Hetzner optimization beats pure Python alternatives.

Retail traders and quantitative analysts

Backtrader · QuantConnect · Zipline

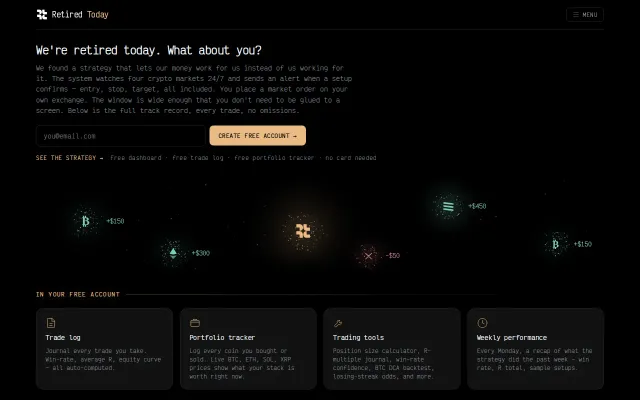

But I didn't want to settle for index funds that hold a lot of under-performing stocks so I've built this tool that allows trading 12000 instruments (stocks, ETFs, metals, real estate, crypto) via statistically proven strategies.

Project is open source, tool is self-hosted, at the very minimum it requires an Alpaca brokerage account, they also provide the necessary market data, alternatively you can use Tiingo or EODHD.

I'm currently running 2 paper trading accounts, fine-tuning parameters like slippage, planning to start ADX on real money soon.

I'm not trying to beat hedge funds and other big players here, instead I'm looking to join them by waiting for a trend to be established (daily time frame, wide stops, long duration trades) and naturally diversifying over all countries and hundreds / thousands of assets.

$99 for Jupyter notebooks when QuantConnect and backtrader offer free backtesting frameworks.

L3 limit order book replay beats OHLC backtesting, but only matters if you're serious quant.

Loop engineering agent that iterates strategies until they beat buy-and-hold.

Transparent crypto signals with full trade log, but the category is saturated.

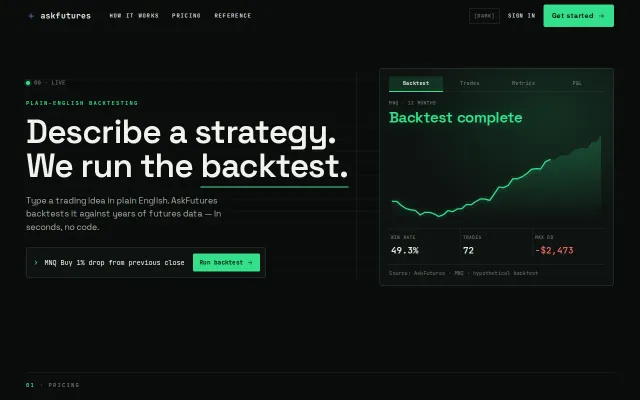

Plain English backtesting when QuantConnect and TradingView already exist.

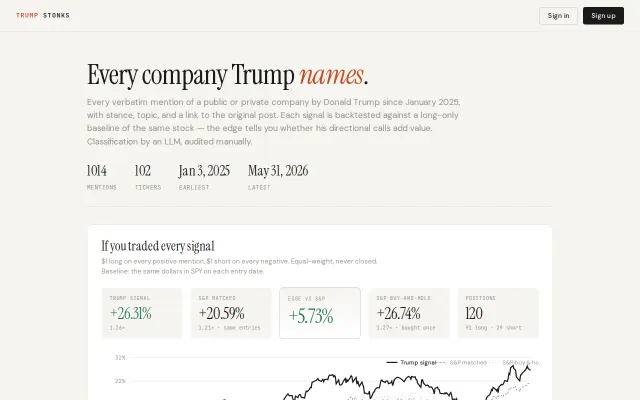

Backtests Trump's company mentions against S&P 500 using LLM-classified sentiment signals.