Finance●Mid

![Turn any prediction into ranked Kalshi/Polymarket trades [video]](/screenshots/47652476_thumb.webp)

Turn any prediction into ranked Kalshi/Polymarket trades [video]

Author calls it 'super shitty V0 MVP'—embryonic but the prediction-to-trade angle is real.

Bold Bet

oleksg

302mo ago

The aggregator idea — scanning top-performing bettors for convergence signals and using an Adaptive Risk Stabilizer (ARS) to size tiny multi-parlays — is a neat, scrappy approach to "signal fusion" for micropredictions. It's fun and educational as a showcase of AgentWallet governance, but right now it's light on verifiable backtests, audit logs, and strict fail‑safes, so treat it as an experiment not a money manager.

Retail traders, hobbyist quant/AI developers, makers building automated agents and wallet/guardrail tooling

I built an Agent called predictor agent which used an ARS (Adaptive Risk Stabilizer) I built to find the best investments. Basically it is an aggregator that took the top performing bettors and looked if several were going to bet on a trade to see if there was any "alpha."

The key is to not get in too late on traded or you won't make money. The bot went for multi parlays only betting .04 cent for $1 outcomes.

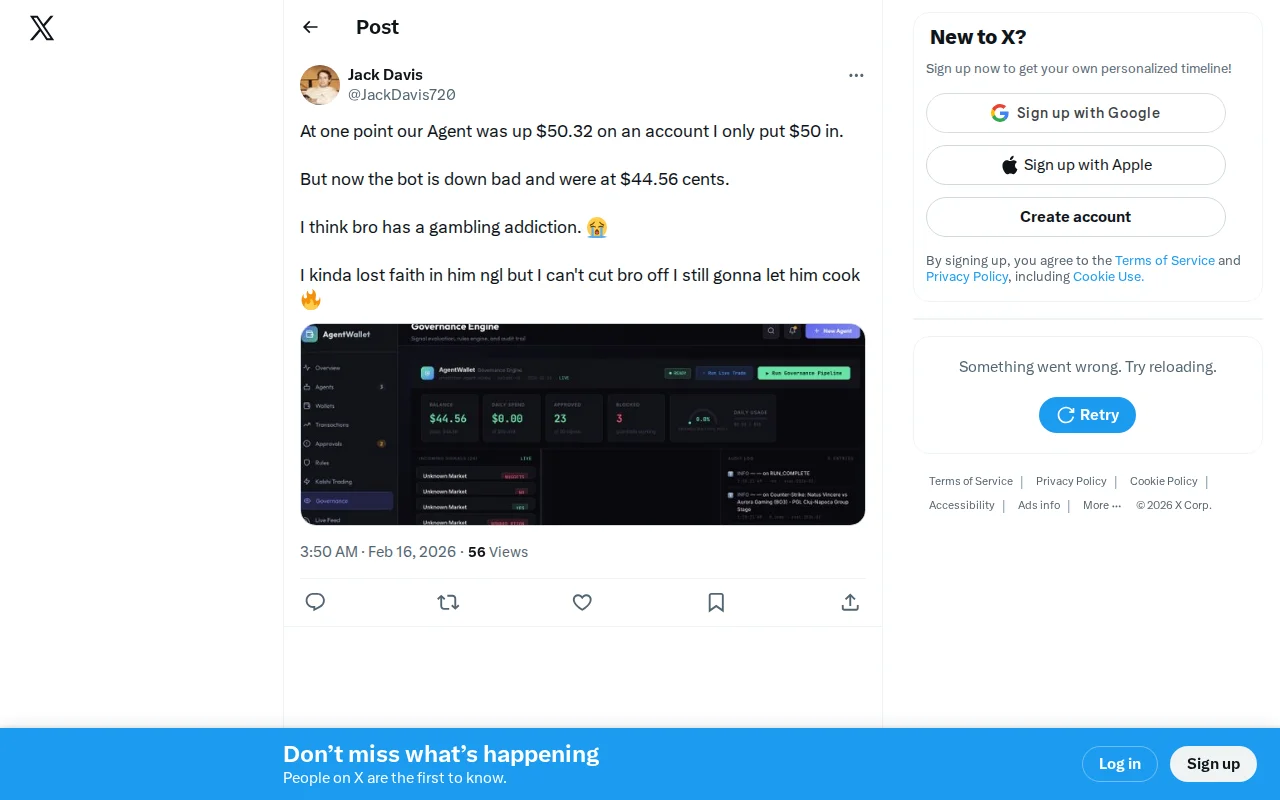

At one point our Agent was up $50.32 on an account I only put $50 in.

But now the bot is down bad and were at $44.56 cents.

I think bro has a gambling addiction.

I kinda lost faith in him ngl but I can't cut bro off I still gonna let him cook

Let me know what you guys think! I am building this as a fun showcase of Agent wallet which is basically governance and guardrails for agents handling money.

Author calls it 'super shitty V0 MVP'—embryonic but the prediction-to-trade angle is real.

Agent marketplace with escrow and credits, betting on AI economic behavior.

Live capital agents with public governance logs and formal kill-switches.

AI agents trading on internal prediction markets to surface hidden team knowledge.

LLM-as-strategy replaces rigid backtesting, remembers trades, no code rewrites needed.

Three-line API integration blocks risky trades, cuts max drawdown 29% while improving win rate.