SaaS●●●Banger

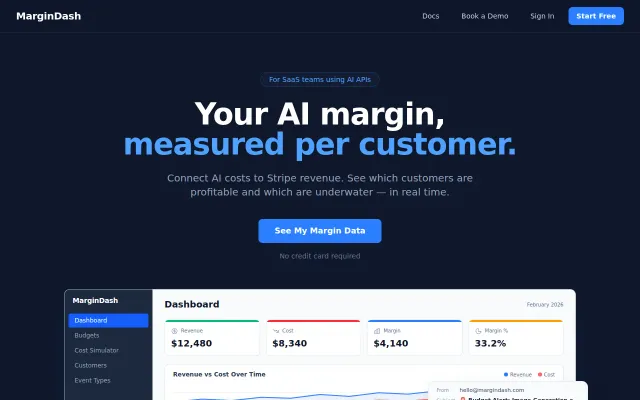

MarginDash – See which AI customers are profitable

Plugs the gap between Stripe and OpenAI bills—finally see which customers are actually profitable.

Solve My ProblemShip It

gdhaliwal23

114mo ago

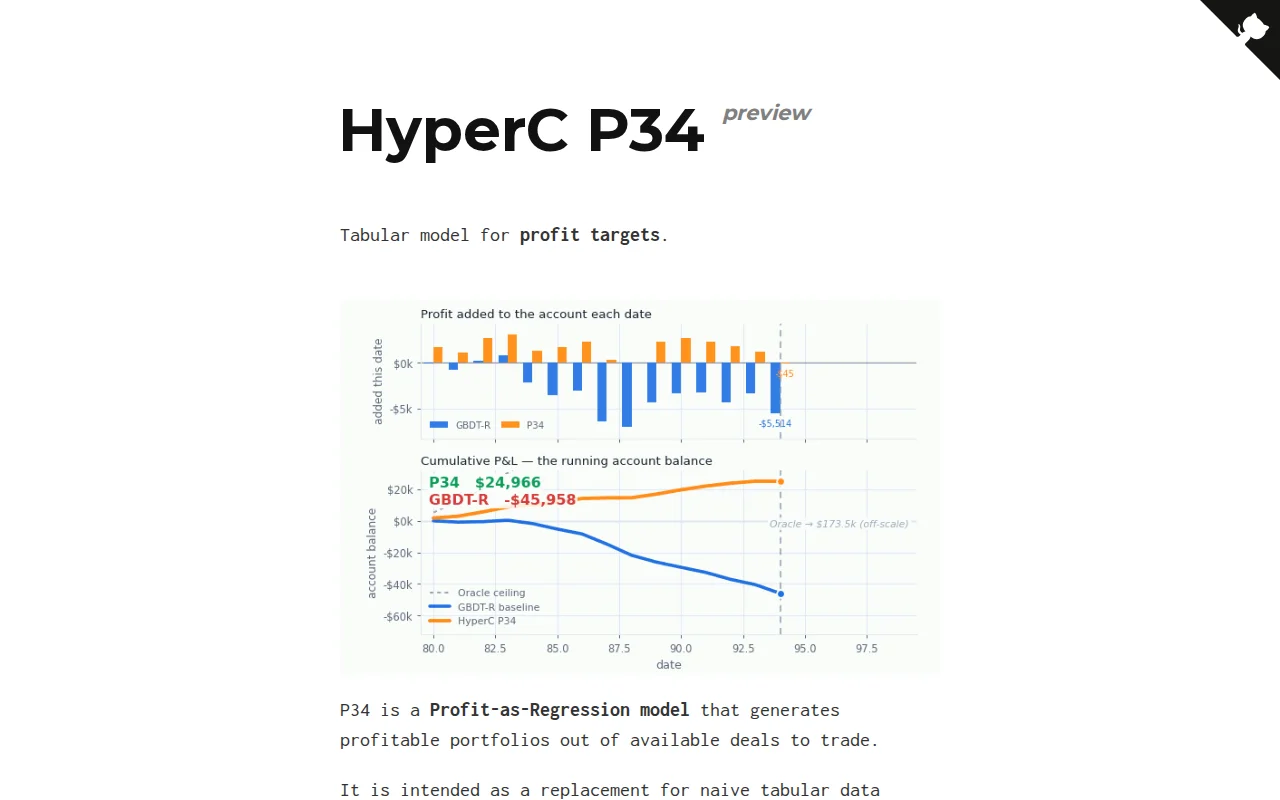

Profit-as-Regression beats naive fitting on synthetic benchmarks with real P&L tracking.

Quant traders, ML practitioners in finance, business decision automation

QuantConnect · PyPortfolioOpt · Backtrader

Plugs the gap between Stripe and OpenAI bills—finally see which customers are actually profitable.

Farming sim profit calculator accounts for regrow cycles and season timing better than wikis.

Turns Garden Horizons crop math from spreadsheets into instant calculator.

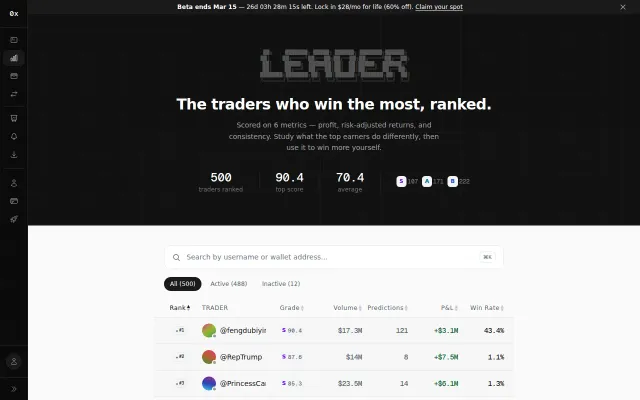

Shows more than raw P&L: six metrics, trader archetypes (DIRECTIONAL, ACCUMULATOR, ALGO_TRADER), persistent grades and filters (active/inactive, search by wallet) make it easy to scan for repeat winners. The UX puts useful columns up front — volume, predictions, win rate and a computed grade — but I want to see the methodology and survivorship controls up front; leaderboard data without clear adjustments can mislead casual users.

Niche calculator for one Roblox game; useful but no staying power beyond active players.

Niche Roblox game calculator with solid Next.js UX; no relevance beyond players.