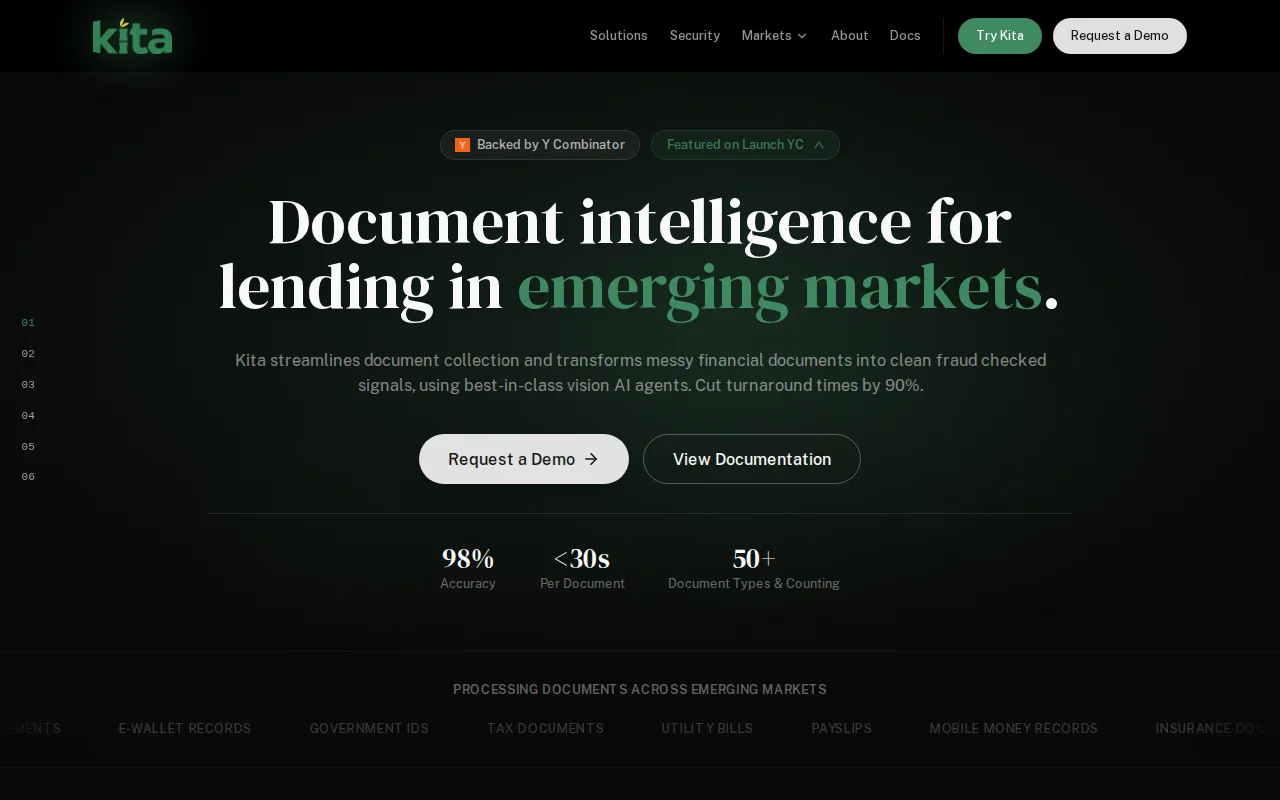

Hey HN! We’re Carmel and Rhea, the founders of Kita (

https://www.usekita.com/). We automate credit review for lenders in emerging markets using VLMs.

In many emerging markets, like the Philippines and Mexico, credit infrastructure is weak. Open finance is still nascent, and credit bureaus are unreliable. So to apply for a loan, lenders rely on borrowers submitting documentation to understand their ability to repay. A borrower can submit financial documents, such as bank statements and payslips, in any format, from pdfs, images of physical documents and screenshots. On top of that, financial documents in these markets are highly unstandardized, with no consistent templates lenders can rely on.

Existing OCR and document AI tools break on these highly variant, messy real-world documents. Generic tools are not built for lending workflows like verification, fraud detection, and risk extraction. As a result, credit teams fall back on manual review, making underwriting slower, more expensive, and more error-prone.

We met before college and stayed best friends. After graduating, Rhea visited Carmel in the Philippines, where we heard firsthand from fintech operators that document-based underwriting was their biggest pain point. We started building together and tested every OCR and document AI tool we could find. They all failed on the messy real-world documents lenders actually receive, and even when extraction worked, they still could not produce the structured financial data or fraud checks lenders needed.

The problem was even bigger than we thought. Across Indonesia, Mexico, the Philippines, South Africa, and even in the US, most of lending can be boiled down to credit analysts looking at documents. In 2025, 13.3T was lended globally, and 90% of those transactions involved document review. This includes in developed markets.

Kita uses VLM-based agents to parse documents, detect fraud, and extract underwriting signals from messy financial files. Today, we support 50+ document types across PDFs, scans, photos, and screenshots. Our pipeline enhances low-quality inputs, extracts structured financial data, and verifies it through cross-document checks, validation against our historical database, and market-specific fraud detection.

Our architecture’s base VLM is model agnostic, and simultaneously, we train language models finetuned to hyperlocalized credit signals in each market, using localized lender data – every new model improves our base layer, and every new market makes our overall stack stronger. We link document-level signals to repayment outcomes, allowing our models to continuously improve fraud detection and risk assessment over time.

Kita Capture is our first document intelligence product for lenders. We’re also launching Kita Credit Agent, which automates borrower follow-up during origination over WhatsApp and email to collect missing documents and complete loan applications.

Kita Capture is free to try (with email signup): https://portal.usekita.com/. Here’s a quick demo: https://www.youtube.com/watch?v=4-t_UhPNAvQ.

We’d love to get feedback from the community, especially if you’ve worked on document AI, fraud detection, or fintech infrastructure. Thanks for reading!